Brand Story – The long-anticipated changes to lease accounting are coming! We’ve been sounding the alarm about this since 2016. In case you’ve been ignoring us (or if you’ve been living under a rock for the past three years), we’ll give you a quick overview.

All leases with a term of more than 12 months must now be present-valued and recorded on the balance sheet as a “Right-to-use” asset, with a corresponding lease liability. This includes leases for partial assets, including your portion of the warehouse or leased office space.

One of the most dramatic aspects of this new standard is the effect on bank covenants for business enterprises. Let’s go through a quick example:

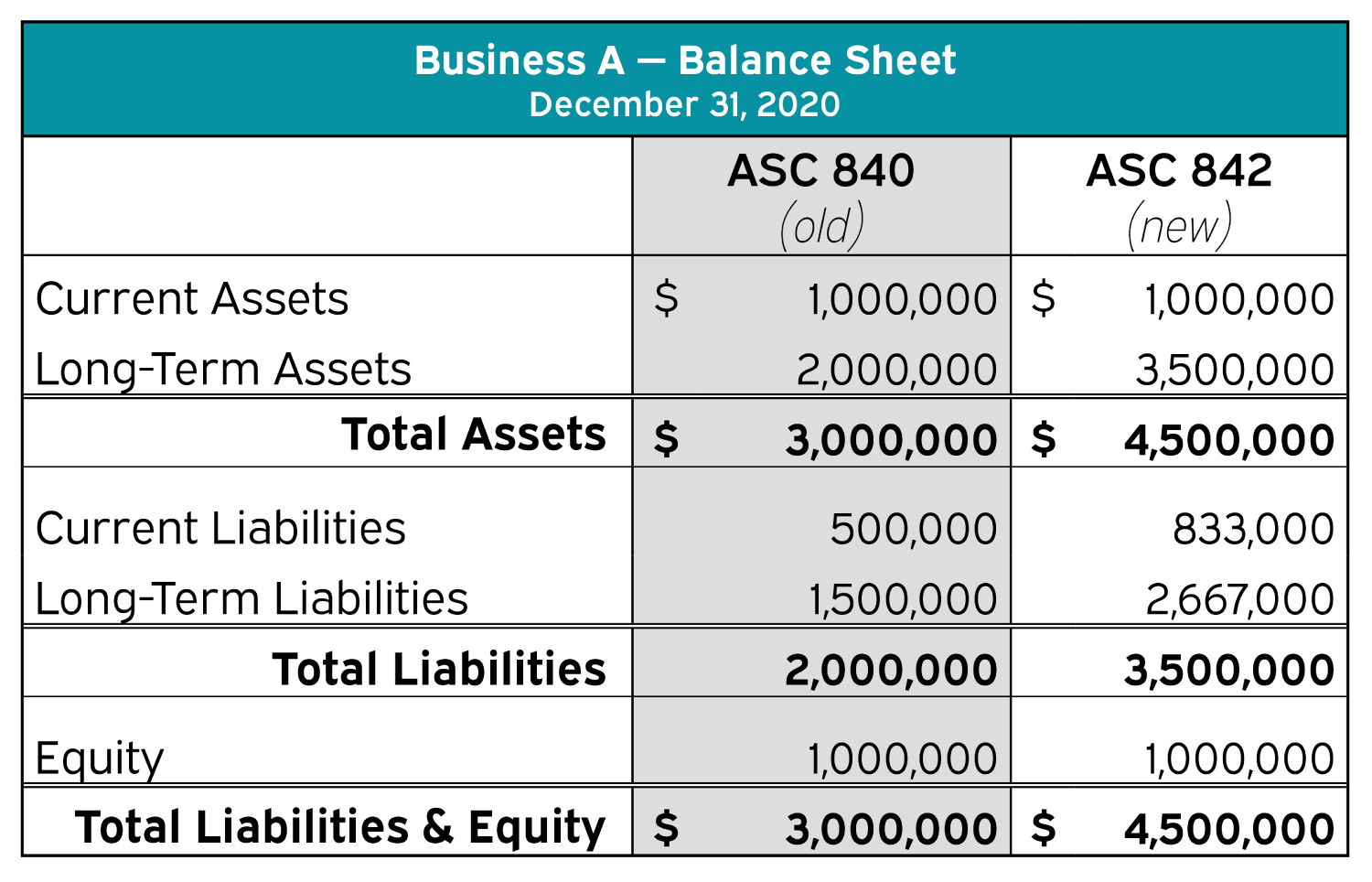

Business A has a building lease that calls for annual payments of $350,000 for five years. Business A‘s incremental borrowing rate is 5.36%. Assuming no other facts, Business A would recognize a Right-to-Use asset of $1,500,000 (noncurrent) and a corresponding lease liability of $1,500,000 (partially current and partially noncurrent).

Here’s what Business A‘s balance sheet might look like, before and after adopting ASC 842:

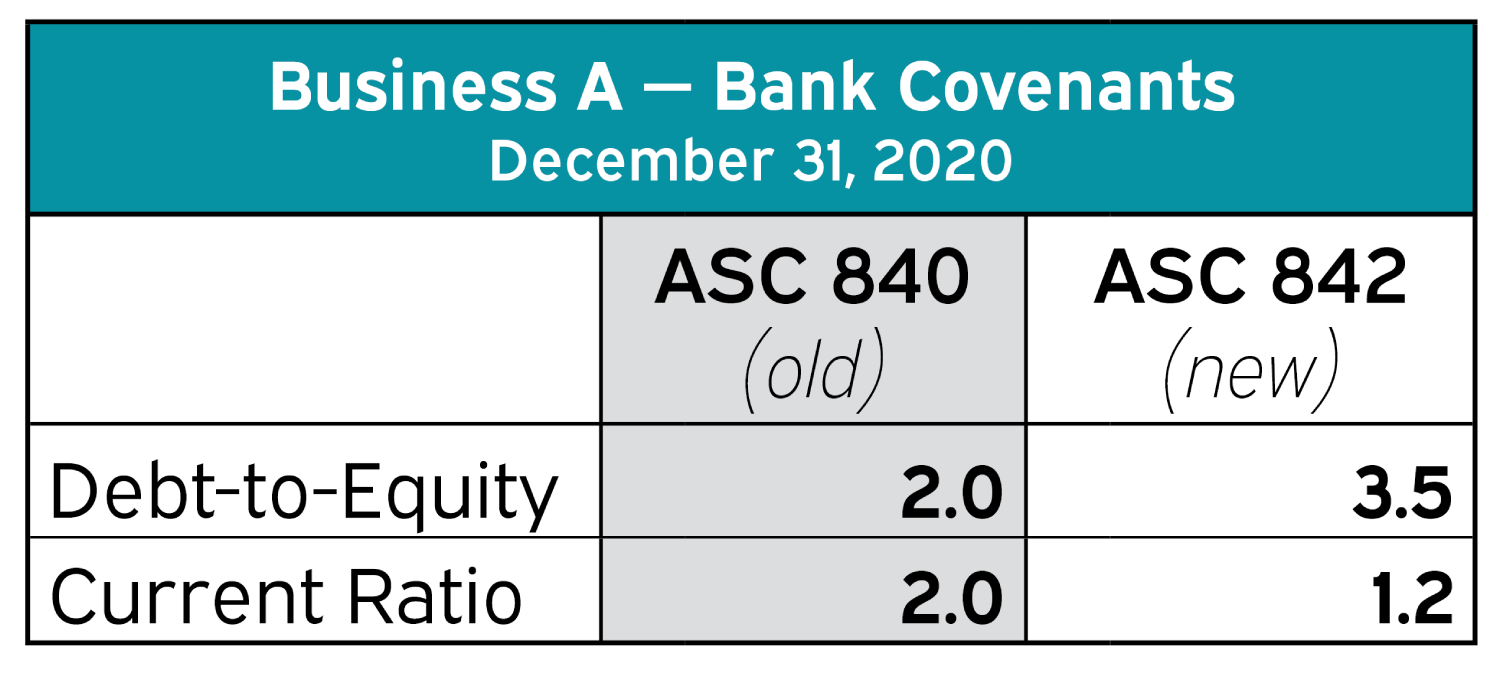

Now let’s take a look at how this change could impact Business A‘s bank covenants:

Now let’s take a look at how this change could impact Business A‘s bank covenants:

As you can see, the adoption of ASC 842, which is required by U.S. GAAP for non-public business entities on their 12/31/20 financial statements, increases the Debt-to-Equity Ratio from 2.0 to 3.5, and decreases the Current Ratio from 2.0 to 1.2.

So what should you do? Our advice to clients and other business owners is twofold.

- Ensure that you understand all of your bank covenants and diligently calculate them at least quarterly. For each quarter, you should consider performing an ASC 842 adoption analysis to see whether you will be in compliance after adoption.

- Request that your banker include a “GAAP As-Is” clause in any new or renewed financing agreements.

You may also consider “renegotiating” related party leases to cover a term of 12 months or less, but keep in mind that your financial institution may not like that type of arrangement on an asset collateralizing bank debt.

If you would like help with implementing ASC 842 or evaluating your covenants contact Senior Manager at Geffen Mesher, Matthew Wright, CPA