It was on May 1, 2015 when Patrick Allen, director of the Oregon Department of Consumer and Business Services, knew that the state’s health insurance market was in trouble.

On that day health insurers file their requested rate changes with the regulator for policies that begin the following year. The requested rate increases were well in the double-digit range.

“When insurers filed rates for 2016 we knew that the performance was bad and that the market was losing a lot of money,” says Allen.

The biggest rate hikes were in the individual health insurance market where people who do not have medical coverage through an employer or government program can buy insurance.

The Affordable Care Act (ACA) greatly expanded the individual market by preventing insurers from declining coverage or charging extra to people with pre-existing conditions. A whole new population of previously uninsured people received coverage in 2014 when the ACA came into effect.

On the face of it, the increased demand for health coverage could have been a financial windfall for Oregon’s health insurers. But the market turmoil that followed was unprecedented in the recent history of the industry.

Two of Oregon’s non-profit health co-ops, Health Republic Insurance and Oregon’s Health CO-OP, went out of business in 2015 and 2016. Lifewise Health Plan left the Oregon market. And Moda Health, one of Oregon’s largest health insurers, required $100 million capital infusion to stay afloat.

Insurers are still reeling from the shake out. But it has led to changes in the marketplace that are a force for good: Health insurers are collaborating more with health care providers to rein in medical costs. Carriers also have a better idea of how to price premiums in the individual market.

Although it is unclear whether financial losses could continue to escalate in 2017, insurers are more hopeful that the market will see more stability next year.

RELATED STORY: THE FAILURE OF FEDERAL GUARANTEES

Moda Health is one insurer that expects improvements in 2017. Last year the company required a $50 million capital infusion from its parent, Moda Inc., and $50 million from its partner Oregon Health & Science University after receiving $78 million less than it anticipated from the ACA’s risk corridor program for costs in 2014 (see sidebar).

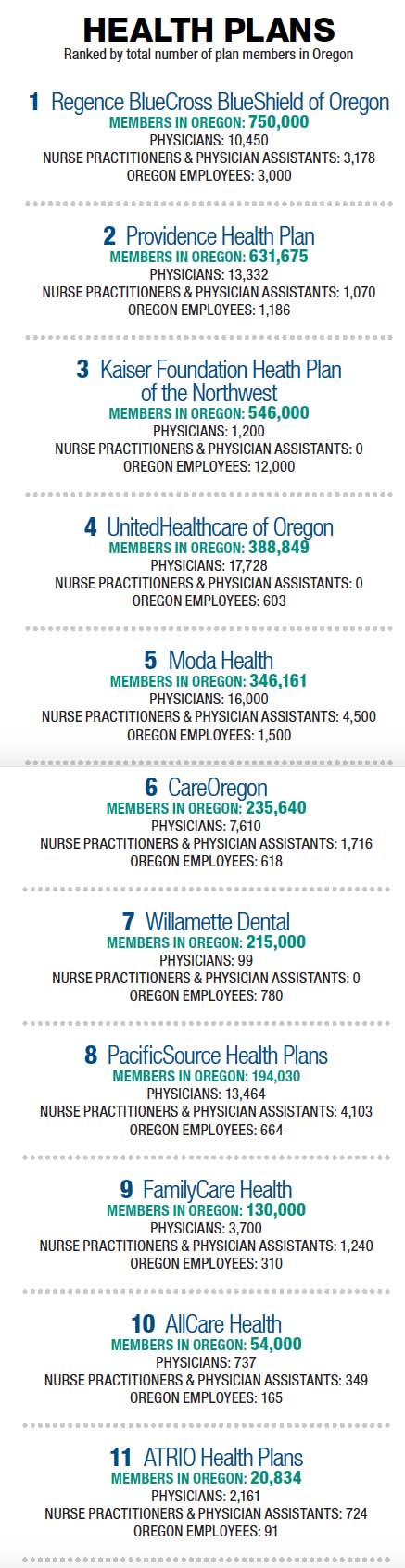

Moda was one of the cheapest carriers selling policies in the individual market in 2014, and as a result had the highest enrollment of any health insurer in the state in the individual market in 2015. A total of 100,962 Oregonians held individual insurance policies with Moda both on and off the exchange in the first quarter of 2015. The next highest enrollment was with Lifewise Health Plan of Oregon (which will exit the Oregon market in 2017) with 36,388 policyholders.

Kraig Anderson, Moda senior vice president and chief actuary, says the company wasn’t trying to be overly aggressive in setting rates. “I hesitate to use the term aggressive. It implies we were trying to buy market share. That was not our intent.”

Setting rates in the individual market was difficult because the company lacked data on the previously uninsured population. “We had to make assumptions about how many would buy insurance, their morbidity, as well as demographics,” says Anderson. “We didn’t know how sick the uninsured would be.”

Miscalculating premiums was an industry-wide problem in the first year of the ACA.

“The entire market was underpriced,” says Allen, adding insurers competed on price because of highly competitive market conditions.

“2017 will be a pivotal year for us. We will have a more effective strategy.”

Moda has increased its rates sharply over the past two years. Its most recently approved rate increase for an individual health plan for 2017 averages nearly 30% higher than in 2016. Anderson says he feels more comfortable that the premiums for 2017 are more reflective of the risk.

“We have a good idea of who is buying insurance in the individual market and the distribution of claims costs,” he says.

To stay profitable Moda has exited the Washington and California health plan markets. It is also focused on a more “integrated approach” to patient care to control costs. In 2017 it will partner with a limited number of health systems in specific geographical areas where it can have better intervention in policyholders’ health care.

An increased effort to control costs is a trend across the health insurance industry.

“2017 will be critical for the market,” says Ken Provencher, CEO of PacificSource. The Springfield-headquartered health insurer has exited several geographical markets, choosing to focus on Portland and central Oregon where it has stronger partnerships with providers, says Provencher.

Like many health insurers, PacificSource is working more closely with a limited number of health care providers to share costs and manage patient care. “2017 will be a pivotal year for us. We will have a more effective strategy.”

Other insurers are seeking to expand areas in which they can manage patient health care costs. One of these companies is Kaiser Permanente, which has traditionally followed the so-called integrated model by working closely with a network of health providers to manage patient care.

Keith Forrester, vice president of sales and business development at Kaiser Permanente, says the insurer plans to increase the use of less expensive modes of treatment, such as telemedicine, to control costs.

Kaiser’s Oregon health plan, Kaiser Foundation Health Plan of the NW, made a profit of $40.9 million in 2016, compared with a 2015 second quarter net loss of $13.2 million. It has managed to increase members in the individual market by 45% to nearly 22,000 in 2016 while turning a profit. It now has the third highest enrollment in the individual market behind Moda with 54,451 members and Providence Health Plan with 104,728 policyholders as of June 30 2016.

Oregon’s health insurance regulator is cautious about forecasting a more stable market in the next couple of years. The exit of thinly capitalized insurance co-ops, Health Republic Insurance and Oregon’s Health CO-OP, has brought some stability. But the department is still concerned about the adequacy of rates.

With some premium increases nearing 30% for individual plans, health insurance is in danger of becoming unaffordable, precisely what the ACA is designed to prevent.

Allen says he is worried about the affordability of health care premiums, but it is a better alternative to sick people going bankrupt because of a lack of coverage. This is what often happened to the uninsured before the ACA came into effect.

Earlier this year the regulator lowered its loss estimate for the state’s health insurance market in 2016 to $42 million from its original estimate of $120 million. The change came after it approved rate increases this year for individual insurance plans that start in 2017.

Based on 2016 data that has come in so far, the agency forecasts losses will be somewhere between $42 million and $120 million, says an agency spokeswoman. Oregon health insurers lost $217 million in 2015, and $36.2 million in 2014.

Allen is unsure whether steep rate hikes are over for now.

“On the one hand, I like to believe that there won’t be more rate increases. As long as the pool of 250,000 people with individual insurance policies stays the same then rate increases will only be driven by health costs,” says Allen.

He cautions the remaining pool of policyholders could get more expensive if a lot of healthy people drop out of the market.

“We still have a couple of years for the market to shake out,” he says.