Investors wary of consumer debt and a tech bubble

The following is part of a series marking the 10 year anniversary of the financial crisis.

Chris Van Dyke, principal at Arnerich Massena, was a director of research at an investment services firm in Chicago during the crisis. He observed the panic that set in among investors after Lehman Brothers failed.

Almost everyone had investment exposure to Lehman Brothers, but it wasn’t just Lehman on the line. Most of the large investment banks were in trouble. Goldman Sachs and Morgan Stanley were under pressure. Goldman Sachs was eventually given a bailout by billionaire investor Warren Buffett. The Treasury Department ended up loaning billions of dollars to hundreds of banks to shore up capital and stimulate lending.

The availability of credit dried up after it became evident how broad the crisis was.

“There was certainly concern about client exposure, what were the dollars at risk. Client portfolios held many different exposures, not just to U.S. banks, but also to banks abroad that were also at risk. It was a global financial crisis. It wasn’t just unique to the United States,” says Van Dyke.

Investors were certainly spooked. It took time before they were willing to take risks again, he says. “It could almost be defined as a trauma. In many instances, both institutional and retail investors expected that it will come again. It took a while, just like after the Great Depression, for individuals to embrace risk and reward and be compensated for it.”

Ten years down the line, that “trauma” has subsided. Van Dyke describes the investment community’s willingness to take risk these days as even “over exuberant.” He points out that less than one-third of traders today actually witnessed the financial crisis. And memories are short. “To quote Mark Twain: ‘History doesn’t repeat itself, but it rhymes.’”

The unprecedented run-up in consumer and government debt is an indicator of the extent to which lending has reestablished itself.

Several years of low interest rates have stoked a borrowing boom that has pushed up consumer debt levels to a record high. The barriers to accessing credit are as low as they have been in the past 10 years. “In history, there were very few timeframes when there have been such low interest rates across so many countries,” says Van Dyke. “It fuels growth in the near term to the detriment of growth in the long term.”

U.S. consumer debt reached a record $3.9 trillion in June 2018, according to Federal Reserve data. That is a 55% increase from June 2007 before the crisis hit.

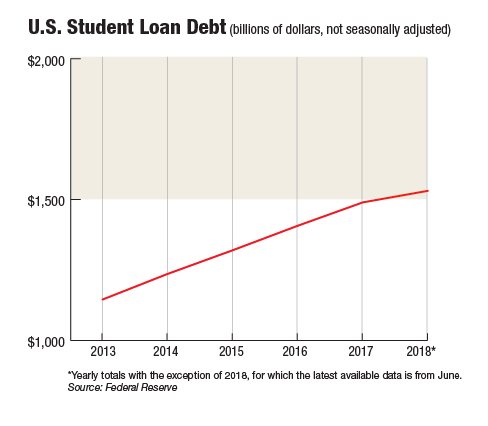

Student loan debt is one the biggest areas of growth for U.S. consumers. It reached a high of $1.5 trillion in June 2018, according to Federal Reserve data. That is around 50% more than U.S. credit card debt. By contrast, mortgage debt as a portion of household debt has stayed relatively stable over the past decade.

Van Dyke does not see the same kind of problems occurring with subprime mortgages that triggered the last financial crisis.

But he is keeping on his eye on other areas of the market that he perceives as risky.

One is the direct lending market. In this kind of peer-to-peer lending, finance companies loan money to individuals for a fixed rate. Investors can invest in these unsecured pools of loans for a return. “Those loans, once yielding 14%, are now in the single digits in terms of yield. You are not getting compensated for this straight credit card-like debt,” says Van Dyke.

Another area he is wary of are investments in high-growth tech companies, such as Facebook, Google and Amazon. These companies have very high valuations that do not reflect their earnings growth potential, he says. “We are looking at more steady cash flow companies where we think there is some good downside protection, but still some decent upside.”

His firm is also pulling back from investments in non-US government debt.

SEE RELATED STORY: ‘THERE IS NO INVESTMENT STRATEGY TO SOLVE THE UNFUNDED LIABILITY’

Transparency has improved in the investment services sector since the crisis, says Van Dyke. “We include full expense transparency, also on our holdings and exposures, derivatives, leverage of underling portfolio – things that weren’t paid as much attention to previously.”

Could a financial crisis of the same magnitude happen again? He thinks it could, though it is impossible to say when. “To have foreseen in 2007, 2008 how calamitous it was would have been truly prescient or prophetic.

“In the last 10 years, people continue to think it is around the corner, yet we continue to see growth and profitability.”

Read more on this series on the financial crisis:

The legacy of the financial crisis 10 years on

‘I didn’t see a lot of the bad stuff until the end’

‘I get the impression everyone thinks another financial crisis is around the corner’

‘Less regulated, non-bank lenders are making high risk corporate loans’

To subscribe to Oregon Business, click here.