Share this article! Thirty years ago last week, we experienced the infamous Black Monday stock market crash. Today, a sell-off of 508 points on the Dow Jones Industrial Average (DJIA) would be slightly over two percent, a regular occurrence during any given year. Back in 1987 it was a 23% decline. The 1987 fall was … Read more

Thirty years ago last week, we experienced the infamous Black Monday stock market crash. Today, a sell-off of 508 points on the Dow Jones Industrial Average (DJIA) would be slightly over two percent, a regular occurrence during any given year.

Back in 1987 it was a 23% decline. The 1987 fall was the worst single-day percentage sell-off in stock market history. The irony of that sell-off is that stocks still finished the year positive.

We share this perspective because of recent concern from clients regarding the strength of the today’s U.S. equity markets. Most major U.S. stock indices are at all-time highs, and over the last 15 months, we have seen very smooth market activity.

As we look forward to the final two months of 2017, history gives us mixed messages, resulting in good, bad and ugly scenarios.

The Good

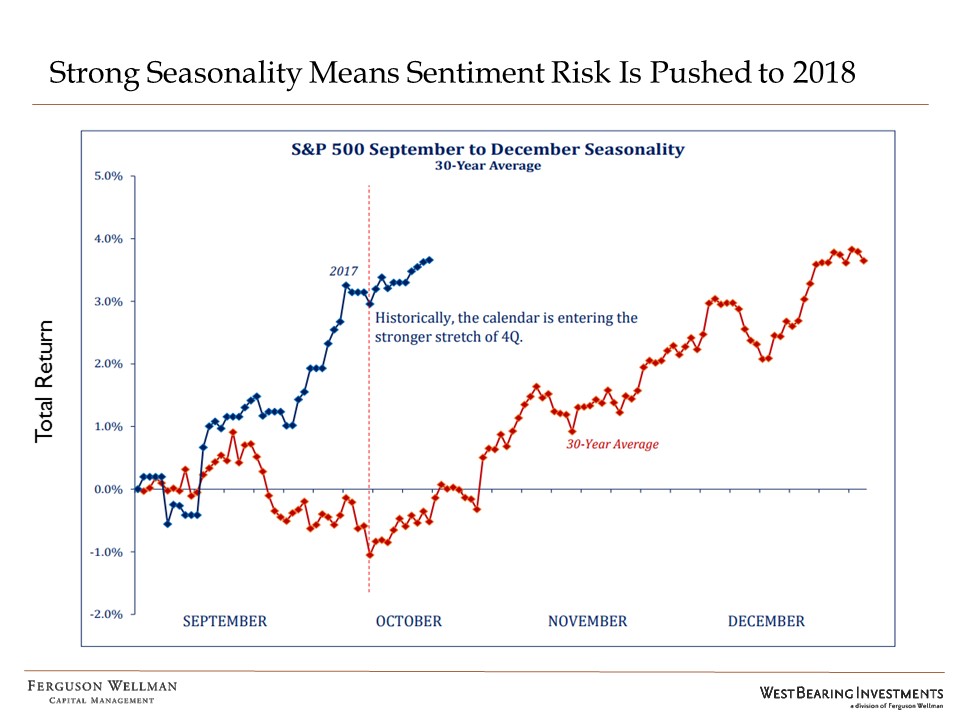

The fourth quarter of any given year is historically the best for equity returns, and performance-to-date has been right on cue, as seen in the chart below.

Source: Strategas

While 2017 has delivered above -average fourth quarter results so far, global economic growth and strong company earnings give us no pause to stay invested for the remained of the year.

The Bad

Over the last 130 years, investors have seen a major drawdown of roughly 13% between August and November on any year ending with a “7.” In most recent memory, we have the 1987 crash, but the worst decline was 40% in 1937.

Drawdowns of this magnitude are common in any given year; however, with just two months left in the year, the calendar is running out of time for this to occur. We don’t see anything on the horizon that would lead to such a major decline in the last two months.

Then again, as Donald Rumsfeld is known for saying, “You can’t know what you don’t know.”

The Ugly

Considerable rhetoric has come out of the Beltway, and Treasury Secretary Mnuchin, added to fuel to the formidable fire of worry earlier this month. He stated that if Congress didn’t pass a major tax plan, the stock market would experience a significant sell-off.

Could this be the catalyst for that infamous decline investors have been waiting for? We believe it is not.

Stocks are up mid-teens not because of a possible tax bill, but because of global economic growth and strong corporate earnings. While investors may get excited over a major reduction in corporate income taxes, we believe this is not priced in stock prices today.

For instance, companies that would benefit more from a reduction of corporate taxes, such as small-cap companies with modest foreign revenue, have lagged the S&P 500. If Congress passes a bill, we believe stocks will certainly rally but if they don’t, the downside will be limited. The hype of cutting taxes we saw after the 2016 election has cooled down dramatically.

The Coin Flip: From the global economy to what’s happening here in Oregon

Two of Portland’s largest companies would nicely benefit from a Congressional tax package, but not significantly. Nike only has 40% of its revenue in the U.S., thus the majority of its business is already being taxed at lower rates. For instance, Nike’s effective tax rate is 16%, so the benefit will only accrue to a minority of its revenue.

Columbia Sportswear is a different story. With over 60% of its business in the U.S., its tax rate is currently at 23%. As a result, a savings from a drop in the corporate rate from 35 percent to 20 percent could warm up their earnings like an insulated jacket on a winter day.

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.