Share this article! Investment pioneer Sir John Templeton coined the phrase, “Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.” After eight-plus years of an equity bull market, a very common question we get from clients is, “When does it end?” While the duration of this market run … Read more

Investment pioneer Sir John Templeton coined the phrase, “Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.”

After eight-plus years of an equity bull market, a very common question we get from clients is, “When does it end?” While the duration of this market run may be extended, bull markets don’t end due to old age.

Below, we will outline why we believe the end of the current bull market is not imminent.

While investors cite record-low volatility and extended valuations as reasons to be worried, we believe that those concerns are overwrought. First, bull markets typically end with a recession, and we do not see a recession within the next couple years.

This eight-year expansion has been the third longest since 1921; only the periods of 1991-2000 and 1961-1969 were longer.

At this juncture, it’s difficult to identify the excess that would bring an end to the current run. Economic growth has been slow and steady at 2-to-2.5 percent, unemployment remains low and there aren’t any inflationary pressures that will cause the Federal Reserve to tap the brakes. While we do believe the Fed will continue to increase interest rates, this will be a slow-and-measured pace. It should not slow the growth rate of the U.S. economic engine, at least in the intermediate term.

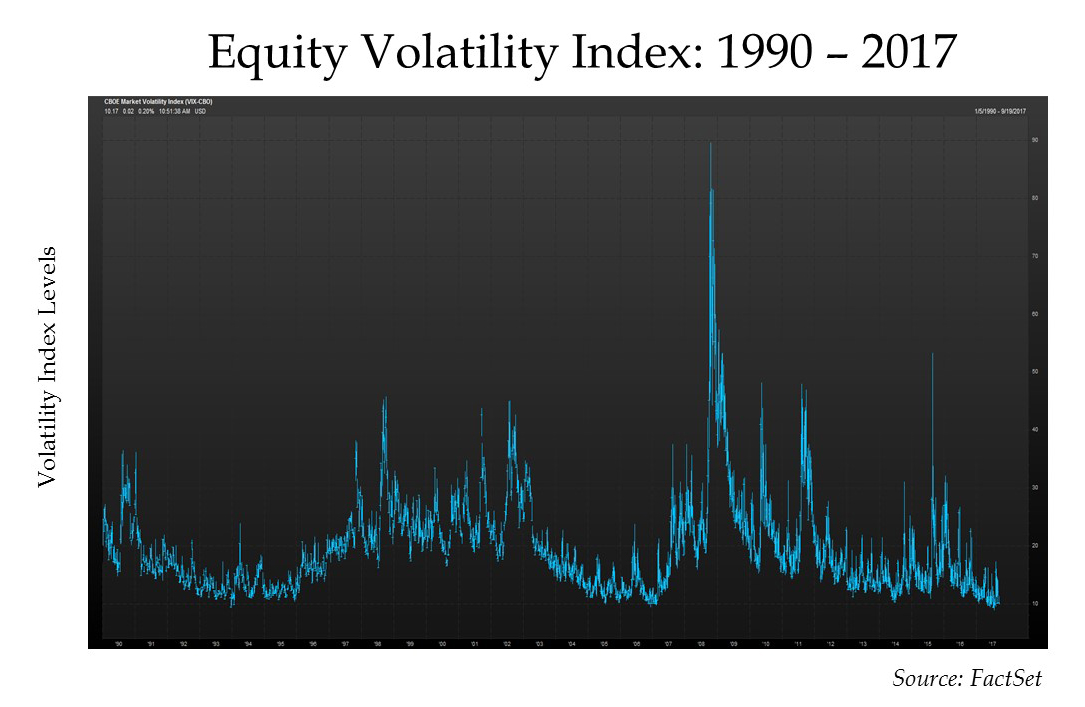

Therefore, one has to look at the equity markets to see if there are any internal warning signs. At present, the two most visible are low volatility and high valuations. While volatility is at historic lows, this relatively calm market is not a sign of the end to the bull market.

The chart below of the Chicago Board Options Exchange Volatility Index (VIX) shows that there can be extended periods of low volatility.

Complacency can certainly precede sell-offs.

Complacency can certainly precede sell-offs.

According to Templeton, complacency has to be a result of optimism or euphoria … and we believe investors are moving into a phase of optimism.

There has been a lot of skepticism regarding this rally and is evident in a few data points. First, investment management surveys show that cash positions are in-line with long-run averages. Second, individual investors continue to sell U.S. stocks. Even after all the stock market optimism we saw at the beginning of the year, investors have sold close to $30 billion in U.S. domestic ETFs and mutual funds in 2017. Only in the first couple weeks of September have we seen the selling stop, but no aggressive buy. This activity is far from euphoric.

Are stocks too expensive to keep going up? We would answer no. While the S&P 500 is trading at 18x earnings, it is not expensive. Though we wouldn’t argue that stocks are cheap, we believe that with earnings growth reaccelerating to 8-to-10 percent, the market can support this valuation. Just as with earnings growth, valuation is contingent on interest rates. With low long-term interest rates, P/E multiples can remain higher for longer.

Is there a “FANG” bubble, similar to the tech bubble in 2000?

Again, our answer is no.

We would argue that while some tech stocks today have extended valuations, the sector in total does not. Specifically, the broad S&P 500 tech sector is trading at 19x earnings compared to 60x earnings in 2000. We believe that company fundamentals are much stronger today than 17 years ago. While famed value investor Julian Robertson sees the S&P 500 getting expensive, he does not believe it applies to the current tech leaders due to their strong growth and high cash generation.

We certainly don’t want to come across as “Pollyannaish” in our views, and we wouldn’t be surprised to see a 5%-to-10% pullback based on a geopolitical event.

Unless that event dramatically alters global economic growth and/or U.S. consumer and business confidence, we believe the bull market will not come to an end under current circumstances.

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.